Future of Mobility

Towards a net zero India

25 March 2025

04 March 2025

Uncertainty grows as strengthening headwinds impact rate of US electric vehicle adoption

The change in administration in the US brings a level of uncertainty regarding the future of the currently proposed passenger car greenhouse gas emissions regulations. Nevertheless, OEMs must still work hard to produce greener cars that appeal to US consumers in a market where full battery electric vehicle adoption rates are slowing. Dan Pridemore, Infineum Industry Liaison Manager for the Americas, explores the latest issues impacting the US personal mobility market and talks about what impacts he expects over the year ahead.

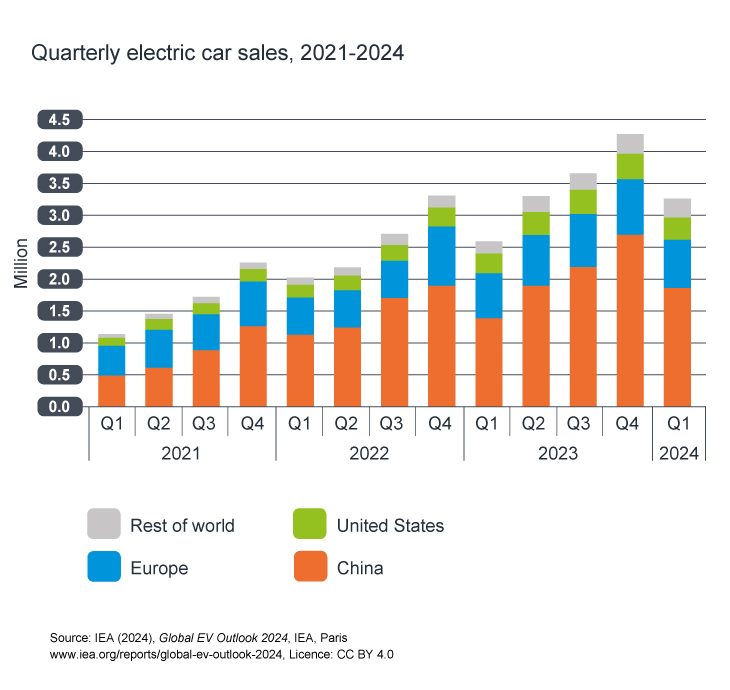

Global automakers are experiencing strengthening headwinds as the US market transitions to battery and plug in hybrid electric vehicles. The US Energy Information Administration (EIA) market snapshot shows recent trends in US light-duty vehicle sales and provides a good baseline to begin our discussion.

In 2024, Battery Electric Vehicles (BEV) sales increased to ~8% and Plug In Hybrid Vehicles (PHEV) accounted for ~2% of US new vehicle sales. Why then the gloomy feeling about the US Market?

A broad range of EV sales forecasts have been published. These forecasts often offer a global perspective and vary depending on the underlaying assumptions. For example, the International Energy Agency (IEA) states that: ‘Every other car sold globally in 2035 is set to be electric, based on today’s energy, climate, and industrial policy settings’. Bloomberg NEF’s long-term outlook sees EVs reaching 73% of global passenger vehicle sales by 2040.

While these forecasts provide a high-level view of BEV and PHEV adoption, sales remain concentrated in a few major markets.

Each regional market has unique characteristics and headwinds, which influence the rate of EV adoption:

Regional views may not fully align with the broader aggregate global forecasts. Let’s look closer at the US regional characteristics and headwinds.

Recent US regulatory policy has been guided by the Biden administration’s climate change concerns and desire to reduce fossil fuel usage.

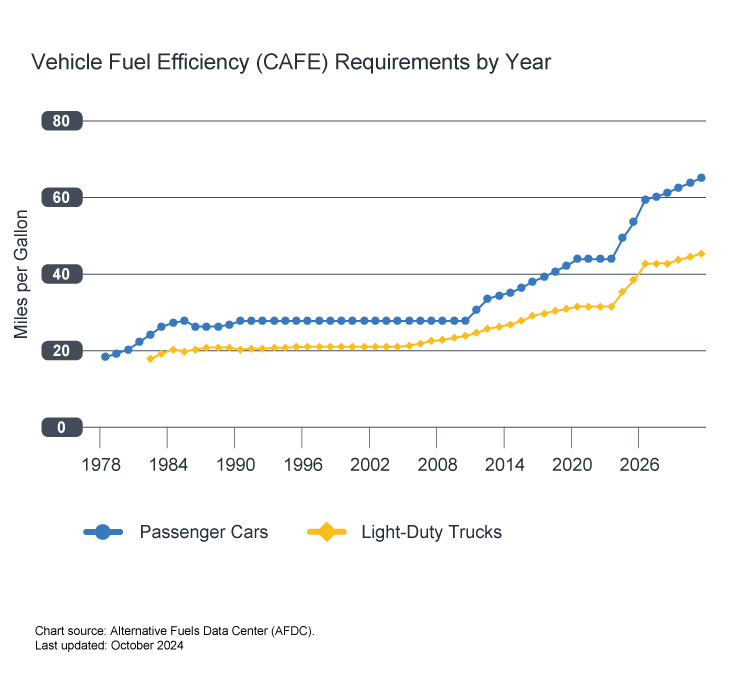

In 2024, the US National Highway Traffic Safety Administration (NHTSA) published new Corporate Average Fuel Economy (CAFE) standards for model year (MY) 2027-2031 light-duty vehicles. These requirements target a combined passenger car and light-duty truck fleet average fuel economy of ~50.4 miles per gallon by MY 2031.

The US Environmental Protection Agency (EPA) published emission regulations for MY 2027 and later light- and medium-duty vehicles targeting a further ~50% reduction in greenhouse gas and other gaseous pollutants and ~90% reduction in tailpipe particulate matter emissions as compared to MY 2026 requirements. While each automaker is allowed to choose the best mix of technologies to achieve these standards, the US EPA projects that battery electric vehicles will account for 30-56% of new light-duty vehicle sales and 20-32% of new medium-duty vehicle sales by 2032.

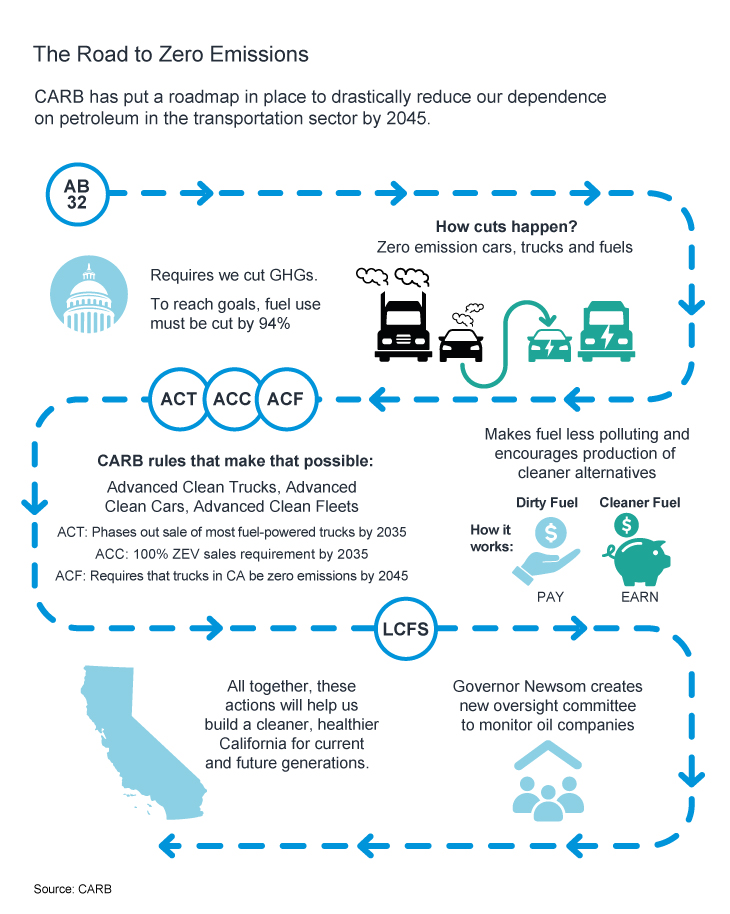

The California Air Resource Board (CARB) has developed a roadmap to zero emissions. This includes regulations targeting the phase out of new sales of fossil fuelled passenger vehicles by 2035, in favour of an 80% BEV/20% PHEV sales mix, and 100% new sales of zero emission trucks by 2045.

The US EPA reinstated the State of California’s waiver allowing it the authority to establish its own stricter emission and fuel economy standards in March 2022. Multiple legal challenges, including the recent US Supreme Court decision not to take up an appeal, have upheld California’s authority to continue this practice.

Additionally, CARB implemented a Low Carbon Fuel Standard (LCFS) targeting a 20% reduction in the carbon intensity of transportation fuels by 2030 for use by PHEV and legacy fleet vehicles. Ethanol, bio-methane, renewable and bio diesel and hydrogen are among the low carbon fuels being promoted.

As a condition of the waiver, the US EPA recently approved California’s Advanced Clean Cars II standards requiring 100% zero emission passenger car new sales by 2035 and certain parts of the other proposed requirements. Other States are allowed to adopt California’s stricter standards if the State is considered in ‘nonattainment’ with federal standards. Seventeen additional States and the District of Columbia have opted to follow California’s standards in recent years. Together these make up some 40% of new light-duty vehicle sales nationally.

Seizing on consumer sentiment, the incoming Trump administration has vowed to eliminate these perceived EV ‘mandates’, revoke the California waiver, eliminate EV and charging infrastructure tax incentives, and impose tariffs on foreign EVs, components, and materials.

With the overall average new vehicle price near $50,000 and the cost of many EVs surpassing $55,000, consumer affordability has emerged as a major concern. Car buying review company, Edmunds.com, reports the number of new vehicle buyers with monthly payments of $1,000 or more is at an all-time high, while the average monthly payment is a record $754 in 4Q2024.

As dealership inventories have risen, automakers have begun offering more promotions, such as cash-back and discounted finance rates. Automotive insights company, J.D. Power, has reported that car buyers received ~$3,400 in incentives during December 2024, an increase of 25% from a year ago.

Affordability is affecting new vehicle buyer behavior. Consumers are leasing more new vehicles to counter higher intertest rates for purchase loans. Edmunds.com estimates that 72% of new EV sales are leased. Many consumers are now choosing smaller cars and SUVs over larger SUVs and pick-up trucks to fit their personal budgets.

The absence of lower priced BEV and PHEV models in this segment contributes to a slowing of the EV adoption rate.

Tesla, for example, recently announced the cancellation of their $25,000 mass-market model.

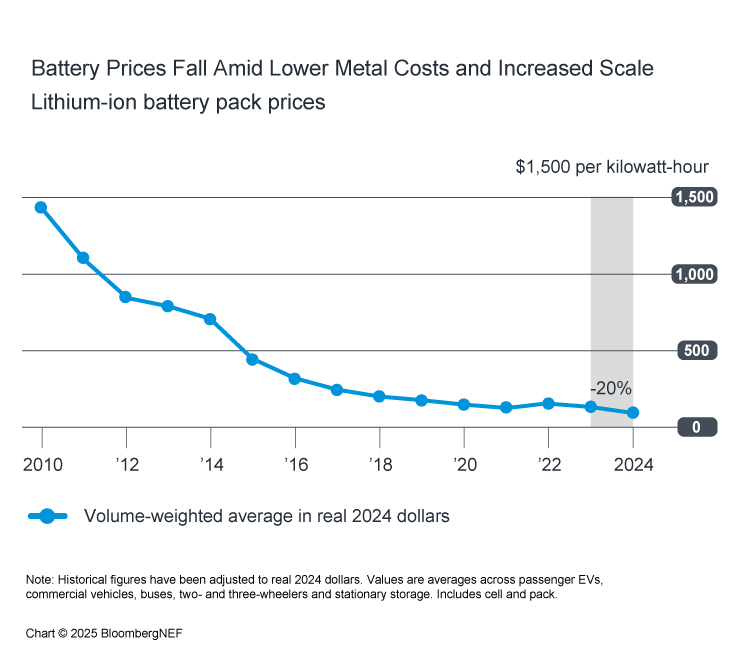

The price differential between conventional and electric vehicles is well recognised. Longer term, automakers are working diligently to eliminate this difference by improving battery cost through advanced battery research and rapid scaling of battery & EV production facilities.

In the short term, automakers are responding by offering attractive leases, higher sales discounts, and revamping supply chains to ensure eligibility for the US Federal tax incentives of up to $7,500 per vehicle.

The US Federal tax incentive was reinstated in the Inflation Reduction Act of 2022. Multiple eligibility requirements were added to receive the incentive, including stipulations on the percentage of critical minerals mined or processed in the US or free trade areas, percentage of battery components manufactured or assembled in the US, and no sourcing of critical minerals or battery components from foreign entities of concern, such as China. These challenging requirements resulted in a limited number of BEV/PHEVs qualifying for a partial or full tax incentive in 2024.

In response to the slowing EV sales rate and rising dealership inventories, automakers are adjusting production.

Ford, for example, has temporarily halted production of their electric F-150 Lightening, delayed or cancelled plans for future vehicles, and is focusing on the production of conventional hybrid vehicles.

While most US consumers charge EVs at home, public charging is needed to address consumer range anxiety and to allow efficient long distance travel across the country.

The US National Renewable Energy Lab (NREL) reports the number of EV charging ports grew by 6.3% in 2Q2024 to ~190,000. The Federal Highway Administration estimates ~1,000 new chargers are being added each week, most of which are in California and the Northeast States.

The type of charging ports being added is also important. Level 1 (L1) chargers are basic, slow charging devices that plug into standard US outlets (120V AC). Level 2 (L2) chargers use 240V AC input to charge at a higher rate than L1 devices; an estimated six to eight times faster. These are the most popular chargers as most US homes can support 240V AC service. Of note in the above graph, direct-current (DC) fast charging ports, also called Level 3 (L3) chargers, are growing by the largest percentage and are capable of adding 10 or more miles per minute in best case scenarios.

Improved availability and affordability of DC fast charging is often seen as the best way to eliminate consumer concerns of BEV driving range and charging times.

While encouraging, NREL estimates that ~28 million charging ports will be needed to service the expected 33 million EVs on the road by 2030. A ramp up of new charging port installations is anticipated in the coming years as grants from the 2021 Bipartisan Infrastructure Law are just now being approved after a stringent due diligence process. Automakers are investing heavily in public charging networks to enable the electric transition. For example, GM recently announced a collaboration with ChargePoint to install up to 500 ultrafast charging stations across the country.

In some markets across the globe, consumer interest in vehicles with gasoline or diesel powered engines is rebounding – particularly as EV affordability concerns continue to influence future purchase decisions. As you can see below, in the US, when we include internal combustion engines (ICE), hybrid electric vehicles (HEV) and PHEV, 88% of future purchases could be expected to contain an ICE.

US consumer sentiment on EVs is mixed, with affordability, driving range, charging time, and availability of charging infrastructure being cited most often as concerns.

Early EV adopters, responsible for driving the rapid adoption rate, tended to be younger, affluent, college-educated, multiple vehicle owners. These demographics allowed many of the above concerns to be overlooked.

Today, these concerns are amplified, and consumers are turning away from EVs and increasingly choosing conventional hybrid vehicles. Looking ahead, automakers will need to work hard to win over the mass market to full BEVs.

Recent reporting supports that new vehicle buyers are gravitating to conventional HEV – those which do not plug into a charging point.

Many consumers feel that these hybrids provide the same fuel economy and emissions advantages as BEV/PHEV without the hassle of external charging. In terms of OEM activity, Toyota has long championed the virtues of HEV, while Ford expects to produce enough HEV to quadruple sales within five years, and GM now says it will offer HEV as part of its product mix.

Moving into 2025, directional improvements in the US automotive market are anticipated, but the proposed actions of the Trump administration are a wildcard. It is expected that affordability should improve, and higher sales incentives, lower finance rates, and improving consumer sentiment are expected to drive total new vehicle sales to exceed 16 million vehicles.

Market forecasters EV Volumes and S&P Global are projecting a modest increase in BEV/PHEV sales of around 11 - 13% of US new vehicle sales, up from some 10.3% in 2024, and HEV are expected to be up to 15% of new vehicle sales. While conventional ICE vehicles retain more than 70% of sales, this forecast is a record low.

In 2025, major advancements are expected to be seen in building out of the EV charging infrastructure and domestic battery and EV production facilities.

The US Energy Department, for example, has finalised a $9.63 billion loan to Ford and SK On to help finance construction of three new battery manufacturing plants, which is the largest loan ever from the government’s Advanced Technology Vehicles Manufacturing loan program.

In addition to meeting stringent regulatory requirements, BEV are also helping automakers to advance technology and development of autonomous vehicles. Steady developments were seen in 2024 with on-the-road testing of robotaxis and self-driving options available in many premium segment vehicles. If consumer acceptance and demand for autonomous vehicles grows exponentially, BEV may become the default preference for vehicle propulsion.

With that said, the incoming Trump administration has announced their intention to eliminate EV subsidies (the federal tax incentive, government loan programs for infrastructure, charging, and domestic production), rescind restrictive California and Federal regulatory standards (publicly called EV mandates), and place substantial tariffs on the import of materials and components needed for EV production as well as on fully assembled EVs. The extent that this occurs and its associated impact on automakers and consumers are unknown, although these measures are anticipated to weigh heavily on the EV adoption rate if fully put into effect. The industry will have to wait and see, with early indications likely to be visible in late 2025.

We will watch with interest to see how the situation evolves as actions taken by the US administration, the automotive industry, and enabling partners impact the trajectory of EV adoption in the US.

Infineum is committed to powering a greener future and are continuing to work closely with industry stakeholder to help ensure the success of the market transition. If you have any questions or need further details, feel free to ask.

Don’t miss our next Future of Mobility article that will focus on Electrification trends in India

Sign up here to receive email alerts so that you never miss out on new Future of Mobility content from Infineum - and make sure you follow Infineum Additives on LinkedIn.

Sign up to receive monthly updates via email